When choosing a health insurance plan, it’s easy to get lost in the sea of acronyms—HMO, EPO, POS, and PPO. Among these, PPO (Preferred Provider Organization) plans are one of the most popular choices, thanks to their flexibility and broader access to healthcare providers. But is a PPO the right fit for you?

In this blog post, we’ll break down what PPO insurance is, how it works, and the key advantages and disadvantages you should consider before signing up.

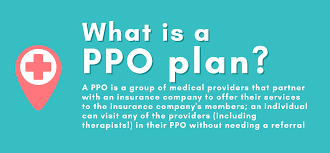

What is PPO Insurance?

PPO (Preferred Provider Organization) insurance is a type of health insurance plan that contracts with a network of medical providers—such as hospitals and doctors—to create a list of preferred providers. Policyholders are encouraged to use this network for their healthcare services.

What sets PPOs apart from other plan types, like HMOs (Health Maintenance Organizations), is that they offer greater flexibility when it comes to choosing healthcare providers and specialists. You do not need a referral from a primary care physician to see a specialist, and you can also seek care outside of the network—although at a higher cost.

How PPO Plans Work

PPO plans operate through a network of contracted providers. Here’s how it typically works:

- In-Network Care: If you visit a doctor or facility within the PPO’s network, you’ll pay less out of pocket.

- Out-of-Network Care: You can still receive care from providers outside the network, but you’ll pay more.

- No Referrals Needed: You can visit any specialist without needing a referral from a primary care doctor.

- Monthly Premiums and Deductibles: PPOs often come with higher premiums and deductibles compared to other plans like HMOs.

Pros of PPO Insurance

1. Greater Flexibility

You have the freedom to visit any healthcare provider, including specialists, without the need for a referral. This is ideal for those who want more control over their healthcare decisions.

2. Out-of-Network Coverage

Unlike HMOs, PPOs cover some portion of the cost if you go outside the network. This is especially helpful if you travel frequently or need access to a wider range of specialists.

3. No Primary Care Gatekeeper

You aren’t required to designate a primary care physician or get approval to see a specialist, which can save time and provide quicker access to specialized care.

4. Larger Provider Network

PPO plans typically have broader networks than HMOs, giving you more choices for healthcare providers.

Cons of PPO Insurance

1. Higher Costs

PPOs generally come with higher monthly premiums, deductibles, and out-of-pocket costs, especially for out-of-network care. This can be a drawback for individuals or families on a tight budget.

2. Complexity in Billing

Because of the ability to go out-of-network, billing can be more complicated. You may have to pay upfront and then file claims for reimbursement, depending on the provider.

3. Potential for Surprise Bills

If you unknowingly receive services from an out-of-network provider (especially in emergency situations), you may end up with surprise medical bills.

4. Less Cost Predictability

Because of the higher variability in provider fees and reimbursement policies, PPO plans can make it more difficult to predict your healthcare spending.

Is a PPO Right for You?

PPO insurance is a solid choice if you:

- Prefer not to be restricted to a small network.

- Frequently need specialist care.

- Travel often and want access to care in different locations.

- Don’t mind paying higher premiums for greater flexibility.

However, if you’re someone who rarely sees doctors, wants low monthly premiums, and doesn’t mind sticking to a limited network, a different type of plan like an HMO might be more suitable.

Final Thoughts

PPO insurance offers freedom and flexibility, making it a popular choice for many Americans. However, the higher cost structure may not be ideal for everyone. Carefully consider your healthcare needs, budget, and personal preferences before choosing a PPO plan.

Still unsure which plan suits you best? Speak with a licensed insurance broker or financial advisor to explore your options in more detail.